QUESTIONS AND ANSWERS ABOUT

THE AICPA PEER REVIEW PROGRAM

February 2024

i

Browse by Section

• Peer Review Enrollment Requirements

• General Information

• Information for Firms Enrolled in the AICPA Peer Review Program

• Choosing a Peer Reviewer (Review Team)

• Preparing for the Review

• Having the Review

• Types of Reports

• Peer Review Committee Consideration and Acceptance

• Implementation Plans and Corrective Actions

• Cooperation with the AICPA Peer Review Program

• Firms That Perform Examinations of Service Organizations

• Interested in Becoming a Peer Reviewer

Table of Contents

INTRODUCTION 1

PEER REVIEW ENROLLMENT REQUIREMENTS 1

What is the AICPA’s practice monitoring requirement? 1

Does my firm have to enroll in a peer review program if it does not have an accounting and

auditing practice? 2

Does my firm have to enroll in a peer review program if the only engagements it performs are

engagements to prepare financial statements under AR-C section 70? 3

Do individuals who are practicing outside of the U.S. have to enroll in a peer review program?

3

Who administers a CPA firm’s peer review? 3

When should my firm enroll in the AICPA Peer Review Program? 4

How can my firm enroll in the AICPA Peer Review Program? 4

Once enrolled, when should my firm expect to have its first peer review? 4

Can my firm change its peer review year-end? 5

GENERAL INFORMATION 5

What are the types of peer reviews? 5

What is a System Review? 5

What is an Engagement Review? 6

How can I find out more about the peer review process? 6

Will information obtained and reported about my peer review be confidential? 6

ii

What is Facilitated State Board Access (FSBA) and how might it affect access to information

about my firm’s peer review? 7

INFORMATION FOR FIRMS ENROLLED IN THE AICPA PEER REVIEW PROGRAM 8

How do I schedule my peer review? 8

Can I have an Engagement Review if my firm has only one audit? 8

What happens when there is a change in my firm’s practice regarding the types of

engagements performed? 9

What is the impact on my firm’s peer review when my firm completes its first audit

engagement after the completion of my Engagement Review? 9

How much will my peer review cost? 10

How can I reduce the costs of my peer review? 10

Can my review be performed somewhere besides my firm’s office? 11

Is my firm required to have a quality control document? 11

Is my firm required to provide copies of individual or firm licenses or registrations to the peer

reviewer? 11

What is a written representation letter? 12

If my firm will undergo a change in firm structure due to a firm name change, dissolution,

merger or purchase/sale, who do I notify about this change and how does it affect my peer

review? 13

What if my firm has received communications relating to allegations or investigations in the

conduct of accounting, auditing or attestation engagements from regulatory, monitoring or

enforcement bodies? 13

How do I determine whether my firm is part of a network? 14

CHOOSING A PEER REVIEWER (REVIEW TEAM) 14

How are review teams assembled to conduct my peer review? 14

What questions should I ask when selecting a reviewer to perform my firm’s review? 15

When should I reach out to potential reviewers to schedule my peer review? 16

How can I find a list of firms interested in performing peer reviews? 17

Who is responsible for making sure the review team is qualified to perform my firm’s peer

review? 17

PREPARING FOR THE REVIEW 18

How should I prepare for my review? 18

When should my firm’s peer review be finished? 18

What if my firm cannot finish its review by the due date? 18

What if my firm’s peer review documents are not submitted to the administering entity by the

due date? 19

What period should my firm’s peer review cover? 19

What if my client does not want their financial information reviewed by the peer reviewer? 20

iii

What is a scope limitation? 20

If my firm is enrolled in the AICPA Peer Review Program, are engagements of employee

benefit plans subject to peer review? 21

When should I contact my System Review team captain and what will he or she want from

me? 22

How should my firm prepare for a subsequent peer review? 23

HAVING THE REVIEW 23

How are engagements selected for a System Review? 23

How are engagements selected for an Engagement Review? 24

TYPES OF REPORTS 25

What types of peer review reports are issued on System Reviews? 25

What types of peer review reports are issued on Engagement Reviews? 26

My firm received an FFC for pervasive issues with complying with the risk assessment

standards (AU-C 315 and 330) on my last peer review. Can I expect similar treatment on my

current peer review? 26

PEER REVIEW COMMITTEE CONSIDERATION AND ACCEPTANCE 27

When are the results of my peer review communicated to me? 27

Who is responsible for submitting review documents to the administering entity? 28

What happens if deficiencies are found by my peer reviewer? 28

What if I don’t agree with the peer reviewer’s conclusions? 28

Can my peer review acceptance letter be withheld until peer review administrative fees are

paid? 29

When are the results of my peer review available for publication? 30

How can I obtain a copy of my firm’s latest peer review report? 30

When is my peer review complete? 30

When would further action(s) be required? 30

What could cause my peer review report to be recalled and what are my responsibilities after

it has been recalled? 30

What happens if it is discovered that a firm that has historically signed “no A&A” affirmations

has been performing engagements subject to peer review? 31

What happens if after my firm’s review is accepted, it is discovered that my firm failed to

include all engagements in its engagement listing provided to the reviewer? 32

What is an implementation plan? 33

What is a corrective action? 33

IMPLEMENTATION PLANS AND CORRECTIVE ACTIONS 34

What happens if I don’t complete the implementation plan? 34

What happens if I don’t complete the corrective action(s)? 34

iv

Can my firm receive both a corrective action and an implementation plan related to the same

peer review? 35

What are some suggested actions that may be required related to a pass with deficiency(ies)

or fail peer review report? 35

What are allowable plans that may be required related to a Finding for Further Consideration?

35

How do the corrective action and implementation plan affect my ability to publicize the results

of my peer review? 35

Should my firm expect an implementation plan for every FFC? 35

Allowable Implementation Plans: System Reviews (PRC 420 Exhibit C) 36

Suggested Corrective Actions: System Reviews (PRC 420 Exhibit D) 37

Allowable Implementation Plans: Engagement Reviews (PRC 420 Exhibit A) 38

Suggested Corrective Actions: Engagement Reviews (PRC 420 Exhibit B) 38

COOPERATION WITH THE AICPA PEER REVIEW PROGRAM 39

What if my firm chooses not to cooperate with the AICPA Peer Review Program? 39

Under what circumstances may a firm’s enrollment be dropped? 39

Under what circumstances may a firm’s enrollment be terminated? 40

Can my firm resign from the AICPA Peer Review Program at any time? 41

If my firm is terminated from the AICPA Peer Review Program, how does the firm get

reenrolled? 41

FIRMS THAT PERFORM EXAMINATIONS 42

OF SERVICE ORGANIZATIONS 42

What are the characteristics of SOC for Service Organizations engagements? 43

I’m having difficulty finding a review team member with appropriate SOC experience. What

are my options? 44

INTERESTED IN BECOMING A PEER REVIEWER 45

What are the benefits of being a peer reviewer? 45

What are the qualifications necessary to become a reviewer? 45

How do I become a peer reviewer? 46

Where can I find more information regarding the training requirements for peer reviewers? 46

APPENDIX A 47

System Review or Engagement Review Determination 47

APPENDIX B 48

Reviewer Qualifications 48

Team Captain or Review Captain 49

Other Peer Reviewer or Reviewing Firm Qualification Considerations 50

APPENDIX C 51

1

QUESTIONS & ANSWERS ABOUT

THE AICPA PEER REVIEW PROGRAM

INTRODUCTION

This question and answer document provides information about the AICPA Peer Review

Program. Included within this document are peer review questions commonly asked by

firms undergoing peer reviews. It will assist those firms to understand requirements

related to peer review and provide other general information and resources about peer

review.

In addition to this document and the resources mentioned, firms can access the peer

review training or the resources web page for additional courses and materials that can

better assist them with preparing for their peer reviews and understanding the peer review

program and process.

Clarified Peer Review Standards (the Standards) can be accessed through Clarified Peer

Review Standards.

Access free Practice Aids Establishing and Maintaining a System of Quality Control for a

CPA Firm’s Accounting and Auditing Practice: aicpa.org/qc4me

Access information regarding the quality management standards as well as news and

resources related to those standards:

aicpa-cima.com/topic/audit-assurance/quality-management

PRIMA

This document contains many references to the Peer Review Integrated Management

Application (PRIMA) system and parts of the peer review process that need to be

completed in PRIMA. PRIMA Help contains an extensive catalog of instructional videos

and articles that describe how to complete these processes within PRIMA. PRIMA Help

can be accessed by clicking on the question mark image in the upper right corner of the

PRIMA Home Page.

Contact us if you have questions about the peer review program!

Back to top

PEER REVIEW ENROLLMENT REQUIREMENTS

What is the AICPA’s practice monitoring requirement?

In order to be admitted or to retain their membership in the AICPA, members of the AICPA

who are engaged in the practice of public accounting in the United States or its territories

are required to be practicing as partners or employees of firms enrolled in an Institute

approved practice monitoring program or, if practicing in firms not eligible to enroll, are

themselves enrolled in such a program:

2

• If the services performed by such a firm or individual are within the scope of the

AICPA’s practice monitoring Standards and

• The firm or individual issues reports purporting to be in accordance with AICPA

professional standards.

Depending on how a CPA firm is legally organized, its partner(s) could have other names,

such as shareholder, member or proprietor.

A member can meet the requirement if his or her firm is enrolled in the AICPA Peer

Review Program (Program).

Firms are required to have their review administered by the National Peer Review

Committee (NPRC) if they meet any of the following criteria:

a. The firm performed or played a substantial role in (as used by the Public Company

Accounting Oversight Board (PCAOB)) an engagement under PCAOB standards

with a period-end during the peer review year.

b. The firm is a provider of quality control materials (QCM) (or affiliated with a provider

of QCM) that are used by firms that it peer reviews.

Firms that are not required to have their review administered by the NPRC may choose

to do so. However, such firms are subject to the NPRC’s administrative fee structure and

should familiarize themselves with that structure prior to making such a decision.

Back to top

Does my firm have to enroll in a peer review program if it does not have an

accounting and auditing practice?

If a firm does not perform services that include issuing reports purporting to be in

accordance with AICPA professional standards, it is not required to enroll in a practice

monitoring program. Firms should consult with their State Board of Accountancy (SBOA)

to determine if the SBOA rules require enrollment in a practice monitoring program even

if your firm does not perform services that include issuing reports.

For purposes of the AICPA Standards for Performing and Reporting on Peer Reviews

(Standards), an accounting and auditing practice is defined as all of a CPA firm’s

engagements performed under the Statements on Auditing Standards (SASs),

Statements on Standards for Accounting and Review Services (SSARSs)*, Statements

on Standards for Attestation Engagements (SSAEs), Government Auditing Standards

(the Yellow Book) issued by the U.S. Government Accountability Office (GAO) and

engagements under PCAOB standards. Engagements covered in the scope of the

Program are those included in the firm’s accounting and auditing practice that are not

subject to PCAOB permanent inspection.

* SSARSs that provide an exemption from those standards in certain situations are excluded from

the definition of an accounting and auditing practice for peer review purposes.

3

Back to top

Does my firm have to enroll in a peer review program if the only engagements it

performs are engagements to prepare financial statements under AR-C section

70?

For purposes of complying with AICPA membership requirements, a firm that only

performs engagements to prepare financial statements under AR-C section 70 is not

required to enroll in a peer review program. For firms already enrolled in the Program,

engagements to prepare financial statements would fall within the scope of peer review.

Independent of AICPA requirements, please note that some SBOAs require firms that

only perform these engagements to enroll in peer review as a licensing requirement. You

should check with the SBOA(s) where you perform such engagements to determine

whether you need to enroll in peer review.

Back to top

Do individuals who are practicing outside of the U.S. have to enroll in a peer

review program?

Individuals practicing in firms outside of the United States or its territories are exempt from

the AICPA practice monitoring program requirement until they return to the United States

or its territories. Please check with your SBOA or other regulatory peer review

requirements as some may require you to have a peer review in this circumstance.

Back to top

Who administers a CPA firm’s peer review?

The Program is administered in cooperation with a state CPA society, group of state CPA

societies and the AICPA Peer Review Board’s (PRB’s) NPRC that elect to participate as

administering entities (AEs). When a CPA firm is enrolled in the Program, its peer review

will be administered by the AE in the state in which the CPA firm’s main office is located

(or, if that state CPA society has elected not to participate, by another AE) or the NPRC.

The PRB approves all AEs.

Firms are required to have their review administered by the NPRC if they meet any of the

following criteria:

a. The firm performed or played a substantial role in (as used by the PCAOB) an

engagement under PCAOB standards with a period-end during the peer review

year.

b. The firm is a provider of QCM (or affiliated with a provider of QCM) that are used

by firms that it peer reviews.

Back to top

4

When should my firm enroll in the AICPA Peer Review Program?

When an individual becomes an AICPA member, and the services provided by his or her

firm (or individual) fall within the scope of the AICPA’s practice monitoring standards, and

the firm (or individual) issues reports purporting to be in accordance with AICPA

Professional Standards, the firm should enroll in the Program by the report date of the

initial engagement.

Back to top

How can my firm enroll in the AICPA Peer Review Program?

A firm should log in to PRIMA and submit its enrollment information. For information on

how to log in to PRIMA, see Getting Started in PRIMA on aicpa.org. By enrolling, a firm

agrees to have a peer review of its accounting and auditing practice once every three

years subsequent to its initial peer review. A firm’s initial review is ordinarily due 18

months from the date it enrolled (or should have enrolled) in the Program. A firm seeking

to enroll in the Program should be in compliance with the Council resolution concerning

form of organization (see AICPA, Professional Standards, ET Appendix B).

Back to top

Once enrolled, when should my firm expect to have its first peer review?

A firm's due date for its initial peer review is ordinarily 18 months from the date it enrolled

in the Program, or should have enrolled, whichever date is earlier.

A firm's subsequent peer review ordinarily has a due date of three years and six months

from the year-end of the previous review. Firms should also check with their SBOA for

any peer review requirements.

In determining the appropriate due date, the firm’s AE will consider the firm’s (or

individual’s) practice, the year-ends of their engagements, the report dates of their

engagements, when the engagements were performed and the number and type of

engagements to be encompassed in the review.

If a firm resigns from the Program and subsequently performs an engagement that

requires a peer review within three years and six months of its prior peer review year-end,

the firm should reenroll in the Program. The due date for the firm’s current review is the

later of the due date originally assigned or 90 days after reenrolling.

If a firm resigns from the Program and subsequently performs an engagement that

requires peer review after its next due date has passed, the firm’s current peer review is

due 18 months from the year-end of the engagement (for financial forecasts, projections,

and agreed upon procedures 18 months from the date of report).

Back to top

5

Can my firm change its peer review year-end?

A firm is expected to maintain the same year-end on subsequent peer reviews.

Circumstances may arise that may cause a firm to want to change its year-end. For

instance, the nature of the firm’s practice may change, or the firm may reevaluate their

current year-end and determine that a different year-end is more practical. In such

situations, a firm may change its year-end only with prior, written approval of the AE.

Back to top

GENERAL INFORMATION

What are the types of peer reviews?

There are two types of peer reviews - System and Engagement. System Reviews focus

on a firm’s system of quality control, and Engagement Reviews focus on work performed

on selected engagements.

Refer to Appendix A for a chart that illustrates which types of engagements require a firm

to have a System Review instead of an Engagement Review.

Back to top

What is a System Review?

A System Review is designed to provide a peer reviewer with a reasonable basis for

expressing an opinion on whether, during the year under review:

a. The reviewed firm’s system of quality control for its accounting and auditing

practice has been designed in accordance with quality control standards

established by the AICPA and

b. The reviewed firm’s quality control policies and procedures were being complied

with to provide the firm with reasonable assurance of performing and reporting in

conformity with applicable professional standards in all material respects.

This type of review is for firms that perform engagements in accordance with the

Statements on Auditing Standards (SASs,) the Government Auditing Standards (Yellow

Book), examinations under the Statements on Standards for Attestation Engagements

(SSAEs) or audit and examination engagements under the PCAOB standards.

Example procedures in a System Review include, but are not limited to:

• interviewing firm personnel,

• examining CPE records,

• examining outside consultations regarding A&A matters,

• examining independence representations and

• testing a reasonable cross-section of the firm’s engagements with a focus on high-

6

risk engagements and significant risk areas.

The scope of the peer review does not encompass other segments of a CPA practice,

such as tax services or management advisory services, except to the extent they are

associated with financial statements, such as reviews of tax provisions and accruals

contained in financial statements.

Back to top

What is an Engagement Review?

The objective of an Engagement Review is to evaluate whether engagements submitted

for review are performed and reported on in conformity with applicable professional

standards in all material respects.

Enrolled firms are eligible to have Engagement Reviews under the following

circumstances:

• The highest level of service does not require a System Review

• Performed under the SSARSs/SSAEs or is another attestation engagement under

PCAOB standards

An Engagement Review consists of reading the financial statements or information

submitted by the reviewed firm and the accountant’s report thereon, together with the

applicable documentation required by professional standards.

An Engagement Review does not provide the review captain with a basis for expressing

any form of assurance on the firm’s system of quality control for its accounting practice.

However, firms eligible for an Engagement Review may elect to have a System Review.

Back to top

How can I find out more about the peer review process?

The AICPA Peer Review web site contains links to resources for peer reviewers, CPA

firms and the public.

In addition, several sections of the AICPA Peer Review Program Manual are available

online at no charge.

Refer to Appendix C for links to available resources.

Back to top

Will information obtained and reported about my peer review be confidential?

A peer review should be conducted in compliance with the confidentiality requirements

set forth in the AICPA Code of Professional Conduct. Information concerning the

reviewed firm or any of its clients or personnel that is obtained as a consequence of the

review is confidential. Peer reviewers may not disclose such information to anyone who

7

is not involved in performing the review or administering the Program or use such

information in any way not related to meeting the objectives of the Program. Also, no

reviewer(s) will have contact with clients of your firm.

The Standards provide for the following information to be disclosed about a firm’s peer

review:

a. The firm’s name and address,

b. The firm’s enrollment in the Program,

c. The date of acceptance and the period covered by the firm’s most recently

accepted peer review and

d. If applicable, whether the firm’s enrollment in the Program has been dropped or

terminated.

Neither the AE nor the AICPA shall make the results of the review available to the public,

except as authorized or permitted by the firm under the following conditions:

• A firm may be a voluntary member of one of the AICPA’s audit quality centers or

sections that has a membership requirement such that certain peer review

documents be open to public inspection.

• A firm may elect not to opt out of the program’s process for voluntary disclosure of

peer review results to SBOAs where the firm’s main office is located.

• A firm may voluntarily instruct their AE to make the peer review results or other

relevant peer review information available to certain other SBOAs.

In such cases, the reviewed firm can allow its peer review results or certain peer review

documents to be made available to the public or to specific entities, such as a SBOA.

In certain instances, these documents may be found in the AICPA’s Public File, which

also contains peer review documents of firms that are PCPS members or those that

voluntarily request to have their peer review documents publicly available.

Back to top

What is Facilitated State Board Access (FSBA) and how might it affect access to

information about my firm’s peer review?

FSBA is a process the AICPA created to help keep up with the evolving changes in the

business and regulatory environments and to address the demand for greater peer review

transparency. This process is intended to create a nationally uniform system through

which CPA firms can satisfy state board or licensing body peer review information

submission requirements, increase transparency and retain control over their peer review

results. The AICPA and CPA state societies are working together to allow this process to

become the primary means by which all SBOAs obtain peer review results. Over time,

this process will help to make submission of your firm’s peer review information easier.

Depending on your state’s requirements, laws and regulations, your firm may have the

option to opt out of this process. Contact your AE for information regarding FSBA

requirements and the submission process for your SBOA.

8

Back to top

INFORMATION FOR FIRMS ENROLLED IN THE AICPA PEER REVIEW PROGRAM

How do I schedule my peer review?

If your firm enrolls in peer review and indicates that it performs services and issues reports

that are within the scope of the AICPA’s practice monitoring program, the firm’s peer

review contact will be notified of the firm’s due date for its peer review.

This notification will occur approximately seven months prior to your review’s due date.

At that time, each firm will be asked to complete its peer review information and

scheduling forms within PRIMA. These forms ask for certain background information of

the firm, such as, but not limited to:

1. Whether the firm has an accounting, auditing or attestation practice as defined in

the Standards,

2. The areas in which the firm practices and any industries in which over 10 percent

of the firm's auditing practice hours are concentrated,

3. Whether the firm performs any audits through a joint venture or partnership

arrangement,

4. The anticipated timing of the review and

5. The team captain/review captain selected to perform the review, if your firm

chooses to select its own review team formed by qualifying firms.

The firm will be asked to provide this information in PRIMA.

During the scheduling process, the team captain will be asked to provide information

regarding the rest of the review team, if applicable. This information should be provided

as soon as reasonably possible, to ensure that the chosen reviewers are qualified and

are approved by the AE so that the scheduling process can be completed. If modifications

to the review team are necessary, they should be communicated to the AE as soon as

they are known.

Back to top

Can I have an Engagement Review if my firm has only one audit?

No. You must have a System Review even if your firm only performs one audit. The

purpose of an audit is to give assurance to third parties. Because of that third-party

reliance, state regulators allow these services to be performed by CPAs only. As such,

the profession has a responsibility to ensure that a CPA firm that performs even one audit

has an adequate system of quality control over its accounting and auditing practice. Such

assurance can only be obtained by reviewing the system of quality control, your firm’s

compliance with that system and by reviewing engagement working papers along with

the report and financial statements. Refer to Appendix A for a chart that illustrates the

engagements that require firms to have a System Review instead of an Engagement

9

Review. Performance of even one of these services would subject your firm to the

applicable type of peer review.

Back to top

What happens when there is a change in my firm’s practice regarding the types of

engagements performed?

You should update the firm’s enrollment information within PRIMA so that the appropriate

type (System or Engagement Review) and the timing of your next peer review can be

determined. See GENERAL INFORMATION for the types of engagements or services

applicable to System or Engagement Reviews. If your firm has been engaged to perform

one or more audit engagements or other engagements that might prompt a System

Review, you should include the number of engagements it has been engaged to perform.

If your firm ceases to perform audit engagements, you should also update the firm’s

enrollment within PRIMA.

Back to top

What is the impact on my firm’s peer review when my firm completes its first

audit engagement after the completion of my Engagement Review?

When a firm, subsequent to the year-end of its Engagement Review, performs an

engagement that would have required the firm to have a System Review, the firm should

(a) immediately notify the AE by updating its enrollment information within PRIMA and (b)

undergo a System Review. Refer to Appendix A for a chart that illustrates which

engagements require firms to have a System Review instead of an Engagement Review.

Performance of even one of these services would subject your firm to the applicable type

of peer review. In this situation, the System Review will ordinarily be due 18 months from

the year-end of the engagement (for financial forecasts, projections and agreed upon

procedures 18 months from the date of report) requiring a System Review or by the firm’s

next scheduled due date, whichever is earlier. However, the AE will consider the firm’s

practice, the year-ends of engagements and when the procedures were performed, and

the number of engagements to be encompassed in the review, as well its judgment, to

determine the appropriate year-end and due date. Firms that fail to immediately inform

the AE of the performance of such an engagement will be required to participate in a

System Review with a peer review year-end that covers the engagement. A firm’s

subsequent peer review ordinarily will be due three years and six months from this peer

review year-end.

The firm should consult with its AE or AICPA staff in the following situation to determine

if the firm will be required to undergo a System Review:

• If the firm is scheduled for an Engagement Review that has not yet commenced

and will issue a report that will make the firm subject to a System Review

Back to top

10

How much will my peer review cost?

The direct cost of a System Review will vary depending on firm size/region, number of

engagements/partners/offices and nature of your firm’s accounting and auditing practice.

Firms with audits in various specialized, complex or high-risk industries, such as banking,

governmental and employee benefit plans will normally pay more than a firm with the

same number of audits that are all in one industry or in lower risk areas. There may be

other factors that influence the cost of a System Review including the design of and

compliance with the firm’s quality control system.

There are also the indirect costs of getting ready for a review that vary based on the

condition of your firm’s existing system of quality control. Many firms are concerned about

these non-chargeable hours. However, if the system of quality control is suitable for your

firm’s practice, the preparation cost should be minimal. If, on the other hand, your firm

finds the opposite is true, it should consider the time well spent since making needed

changes should result in your firm providing better services to its clients, and, in most

cases, providing those services more efficiently.

The estimated cost of an Engagement Review will vary based on the size of the practice

and the number of owners responsible for the issuance of review, compilation and

attestation engagement reports as well as preparation engagements.

The cost also varies based on the type of peer review and peer review team selected to

perform the review. In addition to the review costs that will be incurred every three years,

firms may also pay an annual administrative fee to the AE to cover the costs of running

the program and, in some states, in the review year, fees for scheduling the review and

evaluating the results of the review. For additional cost information, contact your AE.

Finally, firms that are enrolled in the Program and perform engagements requiring the

firm to undergo a System Review are required to pay a national peer review administrative

fee to the AICPA for each year in which they perform such engagements. The fee varies

based on the number of CPAs employed by a firm and will be used to support the

Program’s new and ongoing initiatives to drive audit quality.

Back to top

How can I reduce the costs of my peer review?

The best way to reduce costs is to provide complete, accurate information to the

reviewer(s) early enough, such as 30 to 40 days before the review is set to begin, so it

can be completed by the review due date. Firms that are committed to establishing,

maintaining and improving the quality of their accounting and audit practice tend to have

more efficient peer reviews. Prepare for the review early by making sure everyone in your

firm understands the importance of performing engagements in accordance with

professional standards, and properly documenting engagement planning issues, key

procedures and conclusions. If procedures are properly documented and effectively

organized, it will improve the reviewer’s ability to evaluate what was done without waiting

for engagement staff to recall what they did from memory and should result in less time

to complete the review. In addition, a properly designed environment of quality control

11

and adherence thereto also results in less time devoted to discussing and responding to

matters, findings and deficiencies.

Back to top

Can my review be performed somewhere besides my firm’s office?

There is no requirement for the peer review to be performed at your firm’s office. The peer

reviewer may perform the System or Engagement review remotely.

Back to top

Is my firm required to have a quality control document?

In accordance with Statements on Quality Control Standards (SQCS) No. 8, A Firm’s

System of Quality Control, all firms are required to document their policies and procedures

related to their system of quality control for their accounting and auditing practice. The

extent of the documentation will depend on the size, structure and nature of the firm’s

practice. Documentation may be as simple as a checklist of the firm’s policies and

procedures or as extensive as practice manuals.

The quality control document that is in effect during the peer review year should be

provided to the peer review team.

When establishing and maintaining its system of quality control, sole practitioners and

small to medium-sized firms can also download the practice aids: aicpa.org/qc4me.

Back to top

Is my firm required to provide copies of individual or firm licenses or

registrations to the peer reviewer?

Yes. As a part of a System or Engagement Review, reviewers will make inquiries of your

firm to determine if your firm and its personnel are appropriately licensed as required by

the SBOAs in the state(s) in which your firm and its personnel practice. Your firm should

also submit written representations from the firm’s management indicating compliance

with such required rules and regulations. If your firm is aware of any situation whereby

you are not in compliance with the rules and regulations of the SBOAs or other regulatory

bodies, they should tailor the representation letter to provide information on the areas of

noncompliance.

To support these responses and representations, a reviewer is required to verify:

• The practice unit license (firm license) in the state in which the practice unit is

domiciled (main office is located)

• Individual (personnel) licenses in the state in which the individual primarily

practices public accounting

o For System Reviews, for a sample of appropriate personnel

12

o For Engagement Reviews, for appropriate personnel on engagements

selected

The reviewer will verify the license by requiring your firm to provide documentation from

the licensing authority that the license is appropriate and active during the peer review

year, and through the earlier of reviewed engagements’ issuance dates or the date of

peer review fieldwork. Acceptable documentation includes an original/copy of the license,

print-out from an online license verification system, correspondence from the licensing

authority or other reasonable alternative documentation. The reviewer’s judgment may

be needed to determine what alternative documentation is reasonable.

It is your firm’s responsibility to have understood and complied with its licensing

requirements. Therefore, you should be prepared to respond to the reviewer’s inquiries

and requests for documentation. This is also important for out-of-state firms and individual

licenses when licensing requirements may be more difficult to identify and understand.

When the reviewer deems it appropriate to test out-of-state licenses, your firm is expected

to provide documentation supporting its compliance with, or approach to, out-of-state

licensing requirements. AICPA online CPA mobility provisions may be used to assist the

reviewer in evaluating the firm’s approach to firm and individual out-of-state licensing.

Back to top

What is a written representation letter?

The team captain or review captain obtains written representations from management of

the reviewed firm to describe matters significant to the peer review in order to assist in

the planning and performance of and the reporting on the peer review.

The firm is required to make specific representations (see Exhibit A of PR-C

section 310 .16 and PR-C section 320 .16 ) ) but is not prohibited from making additional

representations. It also may tailor the representation letter as it deems appropriate, as

long as the minimum applicable representations are made to the team captain or review

captain.

The written representations should be addressed to the team captain or review captain

performing the review and be dated the same date as the peer review report which is

usually the date of the exit conference.

The written representations should be signed by individual members of management

whom the team captain, review captain or the AE believes are responsible for and

knowledgeable about, directly or through others in the firm, the matters covered in the

representations, the firm, and its system of quality control. Such members of management

normally include the managing partner and partner in charge of the firm’s system of quality

control.

The reviewing firm and the AE will retain the representation letter until your firm’s

subsequent peer review has been completed. Your firm will be required to submit the

representation letter from the prior review to your peer reviewer in the subsequent peer

13

review.

Additionally, with the firm’s explicit permission, a firm’s written representation letter may

be provided to the AICPA Professional Ethics Division, when there is evidence of an open

ethics investigation.

Back to top

If my firm will undergo a change in firm structure due to a firm name change,

dissolution, merger or purchase/sale, who do I notify about this change and how

does it affect my peer review?

Your firm should contact your AE immediately upon such change. The firm should obtain

a Firm Structure Change Form, complete the applicable section and return the form to

your AE. The AE will submit this form to the AICPA Peer Review Team once all pertinent

information has been received and the form is complete. AICPA staff will determine how

this change will affect your firm’s peer review based on the information provided on the

form and notify your firm of the status.

Back to top

What if my firm has received communications relating to allegations or

investigations in the conduct of accounting, auditing or attestation engagements

from regulatory, monitoring or enforcement bodies?

The reviewed firm should inform the reviewer of communications or summary of

communications from regulatory, monitoring or enforcement bodies relating to allegations

or investigations of deficiencies in the conduct of an accounting, audit or attestation

engagement performed and reported on by the firm, whether the matter relates to the firm

or its personnel, within the three years preceding the firm’s current peer review year-end

and through the date of the exit conference. The information should be in sufficient detail

to consider its effect on the scope of the peer review. In addition, the firm should be able

to submit the actual documentation to the reviewer in those circumstances that the

reviewer deems appropriate. The reviewed firm is not required to submit confidential

documents to the reviewer but should be able to discuss the relevant matters and answer

the reviewer’s questions.

AICPA Peer Review Staff are frequently copied on communications relating to allegations

or investigations from regulatory bodies, such as the Department of Labor or Federal or

State Inspector General’s Offices, sent to or by the AICPA Professional Ethics Division.

Staff will provide copies of these communications to a firm’s peer reviewer if the firm

named in the referral is currently undergoing a peer review. Additionally, a copy will be

provided to a firm’s managing partner and peer review contact. Recipients of required

corrective action letters from the AICPA Professional Ethics Division will be required to

submit evidence that the letter was provided to their firm’s managing partner.

It is also expected that the reviewer and the firm will discuss notifications of restrictions

or limitations on the firm’s or its personnel’s ability to practice public accounting by

14

regulatory, monitoring or enforcement bodies within three years preceding the current

peer review year-end.

The reviewed firm should tailor its representation letter to the team/review captain to

reflect these situations as it deems appropriate.

The peer reviewer and reviewing firm should also notify the relevant AE of any of these

communications relating to allegations or investigations from regulatory, monitoring or

enforcement bodies in the conduct of accounting, audit or attestation engagements

performed by the reviewer. The notifications should occur prior to the peer reviewer or

reviewing firm’s being engaged to perform a peer review, or immediately (if after

engaged). The objective of the reviewer or reviewing firm informing the relevant AE or

AICPA technical staff (as applicable) of such allegations or investigations, limitations or

restrictions, or both, is to enhance the program’s oversight process, which includes

ensuring that peer reviewers and reviewing firms are appropriately qualified to perform

reviews.

Back to top

How do I determine whether my firm is part of a network?

Refer to the Frequently Asked Questions and Sample Case Studies for Implementing

Network Firm Guidance which was developed by the AICPA Professional Ethics group or

contact them directly at [email protected].

Back to top

CHOOSING A PEER REVIEWER (REVIEW TEAM)

How are review teams assembled to conduct my peer review?

The team or review captain will assemble a review team of one or more individuals

depending on the size and nature of your firm’s practice and other factors. The captain

will ensure that all team members possess the necessary qualifications and

competencies to perform assigned responsibilities and that team members are

adequately supervised. All members of the review team will be approved by the AE prior

to the commencement of the peer review.

You may choose the type of review team you would like to conduct your firm’s peer

review.

For any type of review, you have at least two options:

• Firm-On-Firm Review

You hire another qualified CPA firm to conduct the review. This option gives you a

degree of personal assurance that the reviewer’s qualifications fit your firm’s needs.

It also gives you more control over the cost of the review.

15

• Association Review

You ask the association to which your firm belongs to assist in forming a review team.

That association must be authorized by the PRB to assist in the formation of such

review teams.

For Engagement Reviews, besides the two options listed above, there is a third option:

• Committee-Appointed Review Team (CART) Review

For Engagement Reviews in certain states, you may ask the AE to assemble the

review team. Once a team is selected, the AE prepares an engagement letter that

includes an estimate of the number of hours it will take to perform the review and the

reviewer’s billing rates. Billing rates are set by the AE, not by the reviewer. You are

not required to accept reviewers that your AE selects. This option is not available from

all AEs.

Before agreeing to perform a peer review, a reviewer should do the following:

a. Obtain and consider information about the firm to be reviewed, including size,

nature of practice, industry specializations, and levels of service.

b. Assess the reviewer’s own capability and availability to perform the peer review.

c. Consider the review due date to account for adequate time to assess appropriate

responses.

d. Consider the need for additional reviewers with appropriate levels of expertise and

experience to perform the review.

e. Consider the need for individuals with expertise in specialized areas to assist in a

consulting capacity.

Reviewers should not have contact with any client of the reviewed firm in connection with

the peer review without prior approval of the firm and client.

Back to top

What questions should I ask when selecting a reviewer to perform my firm’s

review?

A firm should perform due diligence procedures when selecting and assessing its peer

reviewer, much like the procedures performed when hiring and periodically evaluating a

new employee.

A firm should hire a reviewer who possesses:

• Skills in accounting, auditing and quality control matters,

• Experience in peer reviews,

• Knowledge of the peer review program, and

• A strong belief in improving firm quality.

Examples of questions you should ask when selecting a reviewer include, but are not

limited to:

16

1. How many reviews has the reviewer performed?

2. How much experience does the reviewer have in the industries in which my firm

performs?

3. Will the reviewer be able to complete the review on time, allowing me enough

time to submit any necessary documentation to the AE by my firm's review due

date?

4. Does the reviewer have any references? Can we contact those references and

ask whether they would recommend the reviewer and why?

5. Are there any other value-added services that the reviewer can provide me

during the peer review?

6. What type of Government and/or ERISA audits does the reviewer perform (if

applicable)?

7. Does the reviewer meet all of the qualifications to be a peer reviewer (during the

time of scheduling and expected performance of the review)? See below and

Appendix B regarding training and reviewer qualifications.

8. Has the ability to be a reviewer been limited or restricted or has the reviewer

received notifications of limitations/restrictions on their ability to practice public

accounting by regulatory, monitoring or enforcement bodies?

9. Has the reviewer ever served on a Peer Review Committee or been a RAB

member?

10. Has the reviewer ever attended the annual Peer Review Conference? If so, what

was the last year attended?

11. Has the reviewer ever been oversighted? If so, what were the results?

12. Is the reviewer a member of the GAQC (Governmental Audit Quality Center), the

EBPAQC (Employee Benefit Audit Quality Center), the PCPS (Private

Companies Practice Section), or the CPEA (Center for Plain English

Accounting)?

If you are a member of the Governmental Audit Quality Center and/or the Employee

Benefit Plan Audit Quality Center, keep in mind the membership requirement to have a

quality center member review the GAO, and/or ERISA engagement(s).

For more information and questions, see Questions to Consider when Vetting Prospective

Reviewers.

The suspension, restriction or otherwise disqualification of a reviewer is not a valid reason

for request of an extension of due date by a reviewed firm. In some circumstances in

which the peer review has to be re-performed by another reviewer, the associated cost

may be the responsibility of the reviewed firm. It is the reviewer’s responsibility to

accurately determine and represent its capabilities and qualifications to perform the peer

review. The AICPA’s Guide to Selecting a Quality Peer Reviewer will assist your firm in

understanding the importance of having a quality peer review, hiring a quality peer

reviewer and evaluating peer reviewer qualifications.

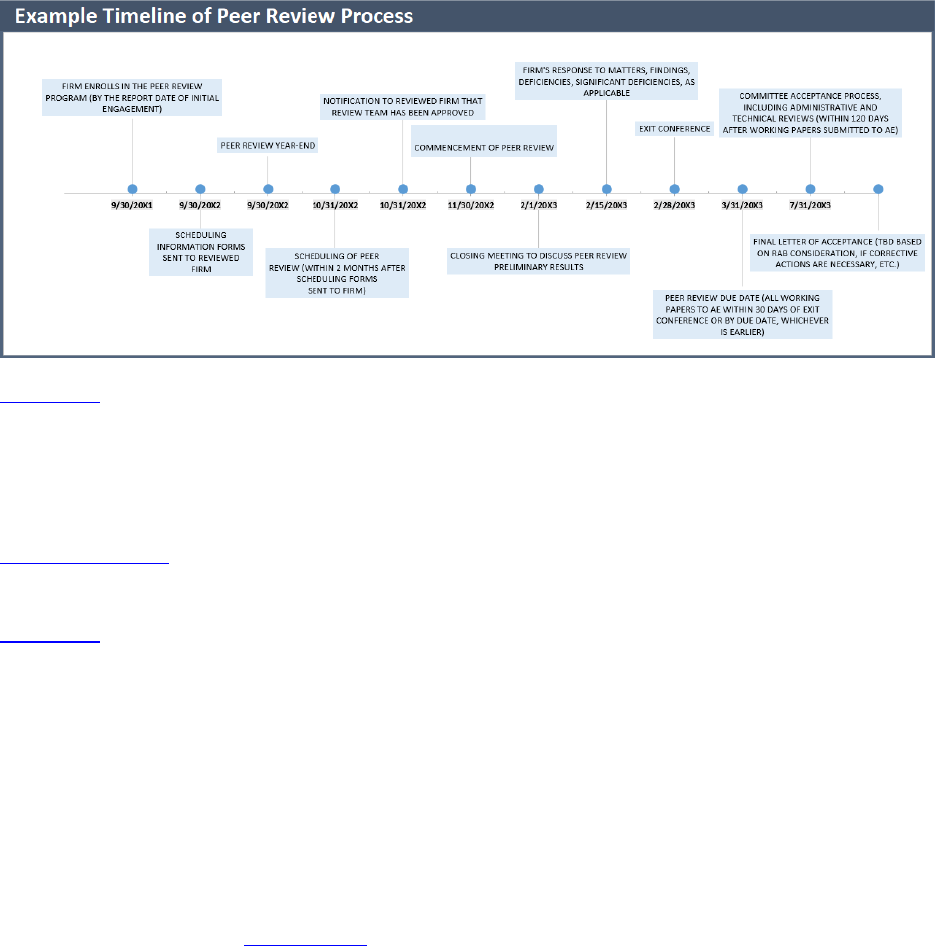

When should I reach out to potential reviewers to schedule my peer review?

As a good practice, your firm should begin to reach out to potential reviewers either before

or at your peer review year-end date, as this will provide your firm and your reviewer

17

adequate time to plan for the peer review. Ordinarily, a peer review is performed within

three to five months following the peer review year-end, but schedules can fill up quickly

so it recommended to reach out sooner rather than later. As a reminder, the below

timeline gives an example of the various steps in the peer review process and is taken

from PR-C Section 100 paragraph A39.

Back to top

How can I find a list of firms interested in performing peer reviews?

The AE may be able to supply you with a list of firms in a geographic area that you specify

that are interested in performing reviews of other firms. The AICPA also maintains a

reviewer search feature on the Program website that you can use to search for reviewers

by state, industry or size of firm.

Back to top

Who is responsible for making sure the review team is qualified to perform my

firm’s peer review?

You should determine if the team captain or review captain has the experience needed

to perform your firm’s peer review. A reviewer/review team not only has to have

experience in the right industries but must also have the right amount and type of

experience. Additionally, all members of the review team have to be approved by the AE

prior to the commencement of the review. In addition, the AE has the authority to

determine whether a reviewer/review team’s experience is sufficient to perform a

particular review. See Appendix B for additional information on reviewer qualification.

If you are a member of the Governmental Audit Quality Center or the Employee Benefit

Plan Audit Quality Center, keep in mind the membership requirement to have a quality

center member review the GAS, and/or ERISA engagement(s).

If a firm chooses to hire its peer reviewer to perform services outside of the scope of peer

review but related to the firm’s accounting and auditing practice, the firm should consider

whether the arrangement would violate independence and objectivity requirements which

18

might prohibit the reviewer from performing the firm’s next peer review.

Back to top

PREPARING FOR THE REVIEW

How should I prepare for my review?

In accordance with Statements on Quality Control Standards (SQCS) No. 8, A Firm’s

System of Quality Control, all firms must establish and maintain appropriate quality control

policies and procedures and comply with those policies and procedures to ensure the

quality of the services they provide to the public. Several publications are available from

the AICPA such as the Standards, the AICPA Peer Review Program Manual, and the

Practice Aids for Establishing and Maintaining a System of Quality Control for a Firm's

Accounting and Auditing Practice.

Back to top

When should my firm’s peer review be finished?

Your firm’s peer review should be finished by its due date. The firm’s due date is reflected:

• On the letter acknowledging your firm’s original enrollment in the Program, or

• In the committee acceptance letter related to your firm’s last peer review.

The due date is the date by which peer review documents, including the report and if

applicable, the letter of response, should be submitted to the AE. To make sure your peer

review is completed on time, you should start the review soon after your firm’s peer review

year-end. You should plan ahead so that the review takes place at a convenient time for

your firm and to allow your reviewer time to properly plan and schedule your review. For

example, if you have a heavy tax practice and your review due date falls between January

and April, you should plan to start the review in September or October to make sure the

review is completed before your busy season begins.

Back to top

What if my firm cannot finish its review by the due date?

If your firm cannot complete its review by the due date, please request an extension in

PRIMA before the due date. Extensions requested after your review’s due date will likely

not be granted. If possible, extensions should be requested at least 60 days before the

due date. However, it is plausible that extensions may be needed due to unforeseen

circumstances within 60 days of the due date. Your explanation to the AE should explain

why your firm cannot complete its review on time and offer an alternative due date for the

review. The AE considers extension requests on a case-by-case basis. Extensions are

not granted simply because a firm believes it needs more time to prepare for the review.

Extensions of a review date by more than three months are rare.

19

In certain circumstances extension requests for due dates may be granted by the AEs,

however, the extensions may not be recognized by your state board of accountancy or

other regulators. Government Auditing Standards require a firm to have an external

quality control review every three years. This three-year period begins with the date your

firm starts fieldwork on its first engagement under GAO Standards. Subsequent reviews

under GAO Standards should be completed within three years after the issuance of the

prior peer review report. If your firm performs governmental audits, don’t forget to take

these requirements and potential changes into account when you request an extension

of your firm’s due date. The GAO and SBOAs are not required to recognize extensions

granted by the AICPA.

Back to top

What if my firm’s peer review documents are not submitted to the administering

entity by the due date?

If the peer review is not completed or documents are not submitted to the AE by the firm’s

due date (including any approved extensions), the firm will receive notifications about the

overdue documents. If the overdue documents are not received after a specified time, the

AE may recommend to the PRB that a hearing be held to determine whether a firm should

be terminated from the Program for failure to cooperate with the AE. If the firm has

cooperated in the completion of the peer review, and the delay is caused by the reviewer,

the firm should communicate this matter to the AE so that appropriate actions can be

taken with regard to the reviewer.

Back to top

What period should my firm’s peer review cover?

The peer review covers a one-year period mutually agreed upon by you and the reviewer

and normally should not change from review to review. Engagements selected for review

in a System Review would generally be those with periods ending during the year under

review, except financial forecasts or projections and agreed upon procedures. Financial

forecasts and/or projections and agreed upon procedures with report dates during the

year under review would be subject to selection. If the current years’ selected

engagement is not completed and a comparable engagement within the peer review year

is not available, the prior years’ engagement will likely be reviewed. If the subsequent

years’ engagement has been completed, the peer review team will consider, based on its

assessment of peer review risk, whether the more recently completed engagement

should be reviewed instead.

The criteria for selecting the peer review year-end and the period to be covered by

Engagement Reviews are the same as those for a System Review.

It is generally anticipated that a firm will keep the same peer review year-end from review

to review. If the prior peer review year-end was not the most convenient for firm personnel

or the most natural year-end for your firm’s practice, send a request to your AE (via

PRIMA) that you be allowed a permanent change to a year-end that is more natural for

20

your firm. Your submission should describe the reasons for your request.

Back to top

What if my client does not want their financial information reviewed by the peer

reviewer?

Firms may have legitimate reasons for excluding an engagement from the scope of peer

reviewers. The following explanations are reasonable for excluding an engagement from

selection in the peer review (this is not intended to be an all-inclusive list):

1. The engagement is subject to litigation.

2. The client will not permit the firm to make the engagement available.

In these situations, the reviewed firm should submit a written statement to the AE prior to

commencement of the review, indicating a) it plans to exclude an engagement(s) from

the peer review selection process, b) the reasons for the exclusion and c) it is requesting

a waiver from a scope limitation in the peer review report. The AE must decide if the

reviewed firms request to exclude an engagement is reasonable and whether the firm

should receive an exemption from the scope limitation.

The PRB has agreed that the following explanations are unacceptable reasons for

excluding an engagement from selection in the peer review (this is not intended to be an

all-inclusive list):

1. The engagement working papers are in a warehouse.

2. The firm no longer performs the audit for that client (and still has access to the

documentation).

3. The firm decided to no longer perform audits.

4. The engagement was selected during the last peer review.

5. The partner on that engagement will not be available when the review is

scheduled.

6. The firm no longer performs engagements in that industry.

If the AE concludes that there is not a legitimate reason for the requested exclusion and

the firm continues to insist on the exclusion, it should be evaluated whether this is a matter

of noncooperation.

Back to top

What is a scope limitation?

There is a presumption that all engagements and other supporting documentation (for

example, CPE records) subject to peer review will be included in the scope of the review.

In rare situations a reviewed firm may have legitimate reasons for excluding certain

engagements or other supporting documentation, for example when an engagement or

an employee’s personnel records are subject to pending litigation.

In these situations, an AE may conclude that scope has been limited due to circumstances

21

beyond the firm’s control and the review team cannot accomplish the objectives of those

procedures through alternate procedures, thus precluding the application of one or more

peer review procedure(s) considered necessary in the circumstances. For example,

ordinarily, the team would be unable to apply alternate procedures if:

• the firm’s only engagement in an industry that must be selected is unavailable for

review and there isn’t an earlier issued engagement that may be able to replace it,

• a significant portion of the firm’s accounting and auditing practice during the year

reviewed had been divested before the review began.

In these circumstances, the team captain or review captain should consider issuing a

report with a peer review rating of pass (with a scope limitation), pass with deficiency (with

a scope limitation), or fail (with a scope limitation), as applicable.

The existence of a scope limitation in and of itself does not result in a report with a peer

review rating of pass with deficiencies or fail; it is in addition to the grade that was

determined to be issued (which is why it is possible to have a report with a grade of pass

(with a scope limitation).

The following explanations are examples of unacceptable reasons for excluding an

engagement from selection in the peer review:

1. The engagement working papers are in a warehouse.

2. The firm no longer performs the audit for that client (but still has access to the

documentation).

3. The firm decided to no longer perform audits.

4. The engagement was selected during the last peer review.

5. The partner on that engagement will not be available when the review is

scheduled.

6. The firm no longer performs engagements in that industry.

If the AE concludes that there is not a legitimate reason for the requested exclusion and

the firm continues to insist on the exclusion, it should be evaluated whether this is a matter

of noncooperation.

Back to top

If my firm is enrolled in the AICPA Peer Review Program, are engagements of

employee benefit plans subject to peer review?

Yes. The Employment Retirement Income Security Act of 1974 contains a requirement

for annual audits of employee benefit plan financial statements by an independent

qualified public accountant. These audits produce reports from the auditor that include

either an opinion in accordance with the auditor’s findings or a statement that an opinion

cannot be expressed. These audited financial statements and auditor’s reports are often

incorporated in a filing with the Department of Labor (DOL) along with the Form 5500

annual report. When included in a filing with the DOL, the auditor’s report is required to

be prepared in accordance with auditing standards generally accepted in the United

States and to reference such standards. As these engagements would be performed

under the Statement on Auditing Standards (SASs), these engagements would be subject

22

to peer review and would require the firm to undergo a system review.

If a firm has historically undergone engagement reviews and decides to perform an audit

of employee benefit plan financial statements subject to DOL filing requirements, the firm

should immediately notify their AE and undergo a System Review. This System Review

would normally be due 18 months from the year-end of the engagement or by the firm’s

next scheduled due date, whichever is earlier. If a firm has never been peer reviewed and

decides to perform an audit of employee benefit plan financial statements (and is required

to be enrolled in the Program), the due date for this initial peer review is ordinarily 18

months from the date the firm enrolled in the Program, or should have enrolled, whichever

date is earlier.

Additionally, a firm may be deemed as failing to cooperate if they omit or misrepresent

information relating to its accounting and auditing practice as defined by the Standards.

If a firm is dropped or terminated for not accurately representing information relating to

its accounting and auditing practice as defined by the Standards, the matter will result in

referral to the AICPA Professional Ethics Division for investigation of a possible violation

of the AICPA Code of Professional Conduct.

Back to top

When should I contact my System Review team captain and what will he or she

want from me?

You should contact your team captain and begin planning the review together early

enough, at least six to nine months prior to the due date, to make sure all documents will

be submitted to the AE by your firm’s due date. Amongst other items, the team captain

will ask for the following items prior to the review:

• The firm’s comprehensive quality control document as required by SQCS No. 8.

• A list of accounting and auditing engagements for all engagements with periods

ending during the year under review (or report dates during the year under review

for financial forecasts and/or projections and agreed upon procedures) regardless

of whether the engagement reports are issued

• A description of the approach taken to ensure a complete and accurate

engagement listing.

• A list of the firm’s professional personnel showing name, position and years of

experience with the firm and in total.

• A copy of the firm’s documentation maintained since its last peer review to

demonstrate compliance with the monitoring element of quality control.

Based on this information, the team captain will make a preliminary selection of the offices

and engagements he or she intends to review. The initial selection of engagements to be

reviewed will be provided no earlier than three weeks before the commencement of the

peer review. This should provide ample time to enable the firm (or office) to assemble the

required client information and engagement documentation before the review team

commences the review. However, at least one engagement from the initial selection to

be reviewed will be provided to the firm once the review commences and not provided to

23

the firm in advance. This engagement should be the firm’s highest level of service and

will not increase the scope of the review.

All engagements with years ending during the peer review year (or report dates during

the year under review for financial forecasts and/or projections and agreed upon

procedures) that are performed and issued by the firm should be available to the team

captain at the start of fieldwork.

Back to top

How should my firm prepare for a subsequent peer review?

In preparing for its next review, your firm should:

• Read the report and any findings from your firm’s previous peer review. If

applicable, be certain that you have taken the proposed actions outlined in your

letter of response from the previous review.

• Perform and document ongoing monitoring procedures to make sure prior

deficiencies have been corrected.

• Review your quality control document making sure your documented policies and

procedures are appropriate based on the size, structure and nature of your firm.

Back to top

HAVING THE REVIEW

How are engagements selected for a System Review?

The Standards require engagements selected by the review team should provide a

reasonable cross section of the reviewed firm’s accounting and auditing practice, with

greater emphasis on those engagements in the practice with higher assessed levels of

peer review risk. Examples of the factors considered when assessing peer review risk at

the engagement level include size, industry area, level of service, personnel (including

turnover, use of merged-in personnel, or personnel not routinely assigned to accounting

and auditing engagements), communications from regulatory, monitoring, or enforcement

bodies; the results of reviews or inspections performed by regulatory or governmental

entities; extent of non-audit services to audit clients, significant clients’ fees to a practice

office(s) and a partner(s) and initial engagements.

In addition, at least one of each of the following types of engagement should be selected

for review:

• Engagements subject to Government Auditing Standards (GAS),

• Audits subject to the Employment Retirement Income Security Act (ERISA),

• Engagement subject to the Federal Deposit Insurance Corporation Improvement

Act (FDICIA) and

• Examinations of service organizations (SOC 1 or SOC 2 engagements).

24

If a firm performs the financial statement audit of one or more entities subject to GAS, at

least one such audit engagement should be selected for review. Additionally, if the firm

performs engagements of entities subject to the Single Audit Act, the reviewer must

evaluate a compliance audit.

Finally, while carrying and non-carrying broker-dealer engagements were scoped out of

peer reviews, the Securities Investor Protection Corporation (SIPC) agreed upon

procedures engagements will remain subject to peer review. Further, the only Broker

Dealers subject to peer review are CFTC-only registered. Due to the limited population

of these BDs, the PRB determined must-select designation for these engagements is not

necessary.

Back to top

How are engagements selected for an Engagement Review?

The review captain or the AE (in a CART review) will select the types of engagements to

be submitted for review in accordance with the following guidelines:

a. One engagement will be selected from each of the following areas of service

performed by the firm:

1. Review of financial statements (performed under SSARSs)

2. Compilation of financial statements, with disclosures (performed under

SSARSs)

3. Compilation of financial statements that omits substantially all disclosures

(performed under SSARSs)

4. Engagements performed under the SSAEs other than examinations

b. One engagement will be selected from each partner, or individual of the firm, if not

a partner, responsible for the issuance of reports listed in item (a).

c. Selection of preparation engagements will only be made in the following instances:

1. One preparation engagement with disclosures (performed under SSARSs)

should be selected when performed by an individual in the firm who does

not perform any engagements included in item (a) or when the firm’s only

engagements with disclosures are preparation engagements.

2. One preparation engagement that omits substantially all disclosures

(performed under SSARSs) should be selected when performed by an

individual within the firm who does not perform any engagements included

in item (a) or when the firms only omit disclosure engagements are

preparation engagements.

3. One preparation engagement should be selected if needed to meet the

requirement in item (d).

d. At least two engagements will be selected for review.

The preceding criteria are not mutually exclusive. One of every type of engagement that

25

a partner, or individual if not a partner, responsible for the issuance of the reports listed

in item (a) in the previous list performs does not have to be reviewed as long as, for the

firm taken as a whole, all types of engagements noted in item (a) in the previous list

performed by the firm are covered.

Back to top

TYPES OF REPORTS

What types of peer review reports are issued on System Reviews?

A team captain on a System Review can issue one of three types of opinions on the firm’s

system of quality control (system): Pass, Pass with Deficiencies or Fail.

Pass

A report with a peer review rating of pass is issued when the team captain concludes that

the firm’s system of quality control for the accounting and auditing practice has been

suitably designed and complied with to provide the firm reasonable assurance of

performing and reporting in conformity with applicable professional standards in all

material respects.

There are no deficiencies or significant deficiencies that affect the nature of the report. In

the event of a scope limitation, a report with a peer review rating of pass (with a scope

limitation) is issued.

Pass with Deficiencies

A report with a peer review rating of pass with deficiencies is issued when the team

captain concludes that the firm’s system of quality control for the accounting and auditing

practice has been suitably designed and complied with to provide the firm with reasonable

assurance of performing and reporting with applicable professional standards in all

material respects with the exception of a certain deficiency or deficiencies that are

described in the report. These deficiencies are conditions related to the firm’s design of

and compliance with its system of quality control that could create a situation in which the

firm would have less than reasonable assurance of performing and/or reporting in

conformity with applicable professional standards in one or more important respects due

to the nature, causes, pattern, or pervasiveness, including the relative importance of the

deficiencies to the quality control system taken as a whole.

In the event of a scope limitation, a report with a peer review rating of pass with

deficiencies (with a scope limitation) is issued.

Fail

A report with a peer review rating of fail is issued when the team captain has identified

significant deficiencies and concludes that the firm’s system of quality control is not

26

suitably designed to provide the firm with reasonable assurance of performing and

reporting in conformity with applicable professional standards in all material respects or

the firm has not complied with its system of quality control to provide the firm with

reasonable assurance of performing and reporting in conformity with applicable

professional standards in all material respects.

In the event of a scope limitation, a report with a peer review rating of fail (with a scope

limitation) is issued.

Back to top

What types of peer review reports are issued on Engagement Reviews?

A review captain on an Engagement Review can issue three types of peer review reports:

Pass, Pass with Deficiencies or Fail.

Pass

A report with a peer review rating of pass is issued when the review captain concludes

that nothing came to his or her attention that caused him or her to believe that the

engagements submitted for review were not performed and reported on in conformity with

applicable professional standards in all material respects. There are no deficiencies that

affect the nature of the report. In the event of a scope limitation, a report with a peer

review rating of pass (with a scope limitation) is issued.

Pass with Deficiencies

A report with a peer review rating of pass with deficiencies is issued when at least one

but not all of the engagements submitted for review contain a deficiency.

In the event of a scope limitation, a report with a peer review rating of pass with

deficiencies (with a scope limitation) is issued.

Fail

A report with a peer review rating of fail is issued when the review captain concludes that

the engagements submitted for review were not performed and/or reported on in

conformity with applicable professional standards in all material respects. A report with a

peer review rating of fail is issued when deficiencies are evident on all of the engagements